4 Funds To Setup To Be Unf***ablewith

Last week I shared the story of how Raymond found out he was overpaying RM 27,000 in his 21 insurance policies using my PMR Template. If you miss it, you can read HERE.

1 of the common question I got these few days was “Ka Hoe, then how much coverage do I need then?”

Today I am going to answer this exact question so that you can “Do The Right Thing” first before “Doing The Thing Right”

Once you know this process, you can start using my PMR tool to choose the best fit and most competitive solution for yourself. This way you won’t waste your money (your blood, sweat and tears) and buy something that does not fit your needs.

Imagine using an umbrella that can only cover half of your body when it rains. You would get wet. That would be frustrating as hell, right? Why would you want that to happen? You will be f***. And the biggest reason most people do that is they don’t know how much emergency fund they need.

Here are 4 funds you need to set up so you can be unf***ablewith. Emergency funds for

A. Job loss and any other – 6 months

B. Hospitalization fund – > RM 1 mil

C. Income replacement fund – 5 years

D. Debt Cancellation and Family Fund – > RM 1 mil

Point A needs no explanation. Everyone needs to put aside cash of at least 3 months (min) and (ideally) 6 months of emergency fund in case we lose our job (yes I’m aware the Covid-19 moratorium took about 3 years). This also accounts for other misc emergencies like car breakdown, mom needing money and etc.

For points B,C and D it will be quite challenging to keep that kind of emergency fund in cash. Imagine trying to save up RM 2-3 Mil in cash. Even if can do it, wouldn’t it be wiser to

1. Take 10% of it and create an emergency fund with the insurance company

2. So that you could invest and work the remaining 90% cash, right?

I know you don’t like insurance. But think of it this way. You like to take loans from the bank right? Even if you don’t, normally we can’t pay 100% cash for our house. So you end up having to take say a RM 500,000 loan and pay the bank RM 2,500/mth for 30 years.

Similarly, I invite you to see insurance as a financial tool to leverage, just like how you leverage on a bank. Can you see the similarities?

1. RM 500,000 Loan Amt is quite similar to RM 500,000 Total Insurance Coverage

2. RM 2,500/mth instalment is quite similar to RM 250/mth insurance premium

3. 30 years loan period is quite similar to a 30-year insurance term policy

Convinced? With that let me share with you this 3-step process to calculate “How much you need to cover to be unf***ablewith?”

Let’s use Mariam’s as an example. Mariam is a Procurement Manager in the wellness industry. She is still single and earning a yearly income of RM 82,524. She has 3 dependents, her Father, Mother and Grandma. She is the only child in her family.

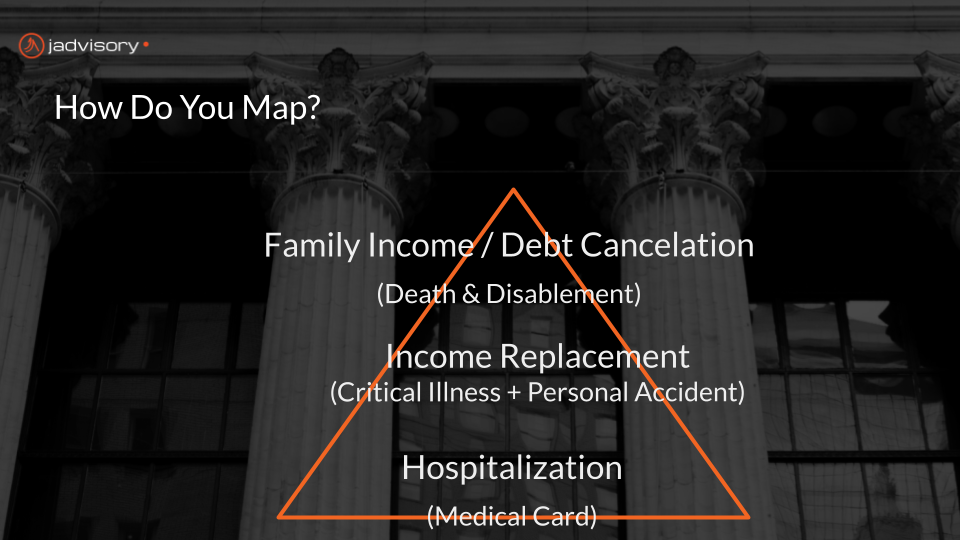

1. Set up your emergency funds in the correct order

Firstly, set up your emergency funds in the correct order. This is how you stack up the emergency funds using my Need Based Insurance Framework.

The lowest is the highest priority. You need to set up first (if you are running on a tight budget). So set up Hospitalization first, followed by Income Replacement and FIDC (Family Income and Debt Cancellation)

2. Match the coverage to the emergency funds

Many of my students ask me “How do I know which coverage is for which emergency funds?” You can refer to the diagram above. Can you see why you need to get these 4 main covers? (I cover this main coverage in my previous mail).

If you are wondering “Hey, how come you didn’t include early critical illness?” I believe these are the 4 main pillars you need to settle first. The rest are variations of these 4, so you can get them when you have extra funds. So

a) Hospitalization -> Medical Card

b) Income Replacement -> Critical Illness and Personal Accident

c) Family Income and Debt Cancellation -> Death and Total Permanent Disability

3. Calculate how much you need for each emergency funds

Start calculating for each emergency fund using the guideline below

a) Hospitalization – For Mariam, since every insurance company starting coverage for hospitalization is RM 1 Mil a year, she started with RM 1 Mil coverage.

Of course the more the better, but be careful of getting too much as the medical insurance cost goes up substantially from age 60 up.

b) Income Replacement – Mariam needed RM 412,620. How did I get this number? You take her annual salary x 5. Why?

The guiding question we ask is “If you were to diagnose with a critical illness, how long you need to stop work before you can recover?”

c) Family Income and Debt Cancellation – For this last emergency fund, Mariam breaks it down further into 4 sub-categories

i) Debts – What is the total outstanding of all her loans so that her dependents are not burdened by it when she ‘goes’? She has RM 199,000 in debts

ii) Final Expenses – This consists of her Burial cost and Estate Administration cost. What it means is when Mariam passes away, does she have funds to take care of the “going away” (burial or cremation) cost?

And have Mariam prepare the emergency funds for the lawyers to be able to transfer all her assets to her loved ones? This came up to RM 116,000

iii) Legacy – any donation she likes to give as religious donations, charity or to loved ones. Mariam does not have any need here yet.

iv) Family Expenses – how much emergency fund does Mariam need to prepare when she is no longer around to ensure her dependents are provided for?

Using our PMR calculator v4, Mariam needed RM 710,000 to provide for her parents and grandma’s daily expenses, allowance and savings for the next 25 years.

So in conclusion…

So in conclusion these are the emergency funds Mariam needed (when you put everything together)

1. Hospitalization – Medical Card of RM 1 Mil

2. Income Replacement – Critical Illness of RM 412,000

3. Income Replacement – Personal Accident of RM 412,000

4. Family Income and Debt Cancellation – Death and Total Permanent Disability of RM 1,025,000

Do you start to feel unf***ablewith when you can set up these emergency funds? Or do you feel more confused than before?

If you are still wondering how, you can join us in our next J Advisory Community Webinar below – How to save RM 27,000 a year and maximize my coverage 5x?

1) Find out are your current existing policies under-optimized.

2) Uncover how to calculate your emergency funds so you feel unf***ablewith

3) Discover examples of wholesale insurance that doesn’t cost an arm and a leg

4) Free gift of PMR Template v4 worth RM 997

Can’t wait, right? Register now.

Whenever you’re ready, here are 3 ways I can help you to improve your cash flow and double your wealth:

- If you’re still looking for ways to improve your cash flow and double your wealth, I’d recommend starting with

-> Ice Jar – The world’s simplest money management system. This is really the foundation to improve your cash flow and double your wealth. Join 830+ students here

-> Double Your Networth – Join 100+ students go through 4 days intensive webinar to fully understand and apply my 5-step DYN Framework to double your wealth and retire 5-10 years earlier.

- Meet up and clarify your doubts with our coaches.

If you are unsure of where and how to move forward or you are feeling stuck, you can sign up for a complimentary Discovery Call with our coaches HERE.

- Let’s stay connected on social media.

Tune in to my Linkedin, Instagram and Facebook profiles

[Linkedin] [Instagram] [Facebook]

DISCLAIMER – All strategies listed here are not a recommendation nor advise. The article is written purely for the purpose of education and journaling only. The content of this article is an expression of my opinion and should not be taken as a professional advise. If you are seeking professional advise, please consult me personally . You should do your own research and/or seek an expert’s advice when overcoming your circumstances