3-Step Process To Identify Are You Overpaying Your Insurance

Today, I’m going to share with you a 3-step process to identify “Are you overpaying your insurance?”

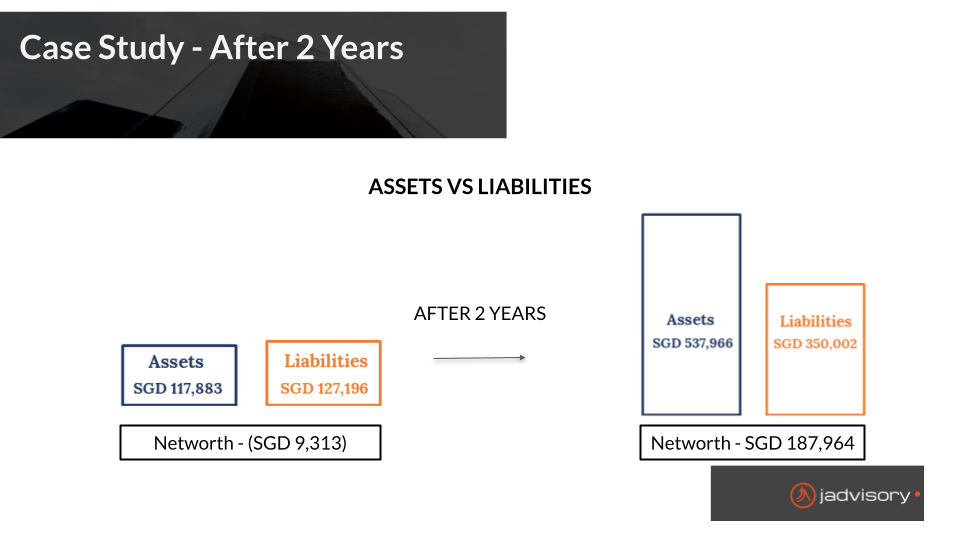

This is the story of Raymond, an IT professional working in Singapore who almost went bankrupt. Thankfully for his job and meeting me in time, he could multiply his wealth 180x in 2 years (from a deficit of SGD9k to SGD 180k Wow!)

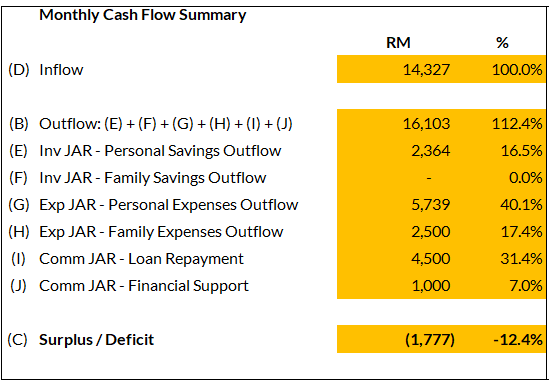

Raymond was suffering an SGD 2k/mth deficit. That prompted him to reach out. Once we went through his ICE JAR and Financial Compass, we found out

- He was overspending SGD 3,239/mth

- He was over-paying on his credit card and 2 personal loans (over-committed)

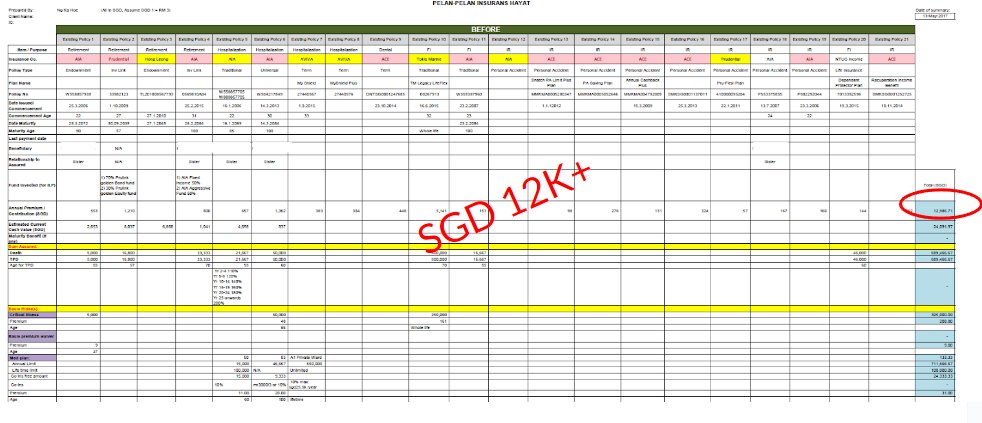

- He was over-paying his 21 insurance policies (over-invest)

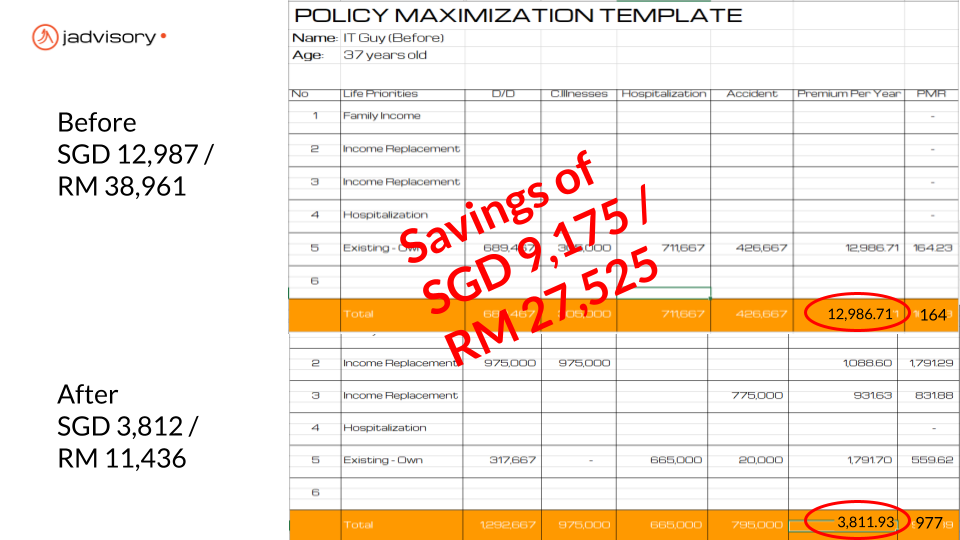

Today I will cover item 3 as Raymond complains he does not have any free cash to invest. Once we use the PMR Template he can see why. He did not realize his good intention of forced savings, led him to overpay 27k a year on his 21 insurance policies.

You see the reason why he forces himself to save is because Raymond is a high-risk taker. He invested in a business his friend pitch him. He likes to trade in forex. So he feels he balances out should the business and his high-risk investment fail. At least he still has some savings. Little did he know his savings were only growing at 3-4% per year while his debts were growing at 18-24% per year. This was the main reason that cause him to be bankrupt (technically)

Are you having similar symptoms like Raymond?

Do you start noticing you are not saving enough money?

Or do you start to notice your assets stop growing?

Don’t worry, follow this 3-step process to find out “Can you cover more by paying less?”. Download the PMR Template and

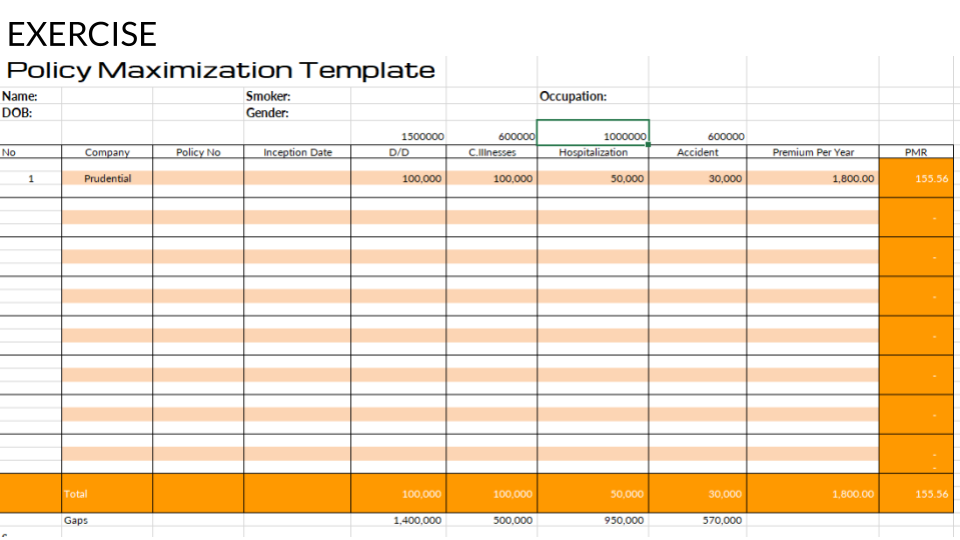

- List out all your insurance policies

Start listing down all your insurance policies from either your hardcopy policy or you can log into your internet insurance portal. The 4 main coverage you must have are

- Death & Disablement coverage

- Critical Illness coverage

- Personal Accident coverage

- Hospitalization coverage

- Match the latest premiums with the correct insurance

Once you listed down all your insurance policies, key in the latest insurance premium. Chances are if you have not reviewed your policy for a long time, the premiums would have changed after a couple of years. So if you are paying RM 150 a month, just multiply it by 12 and fill in RM 1,800 below

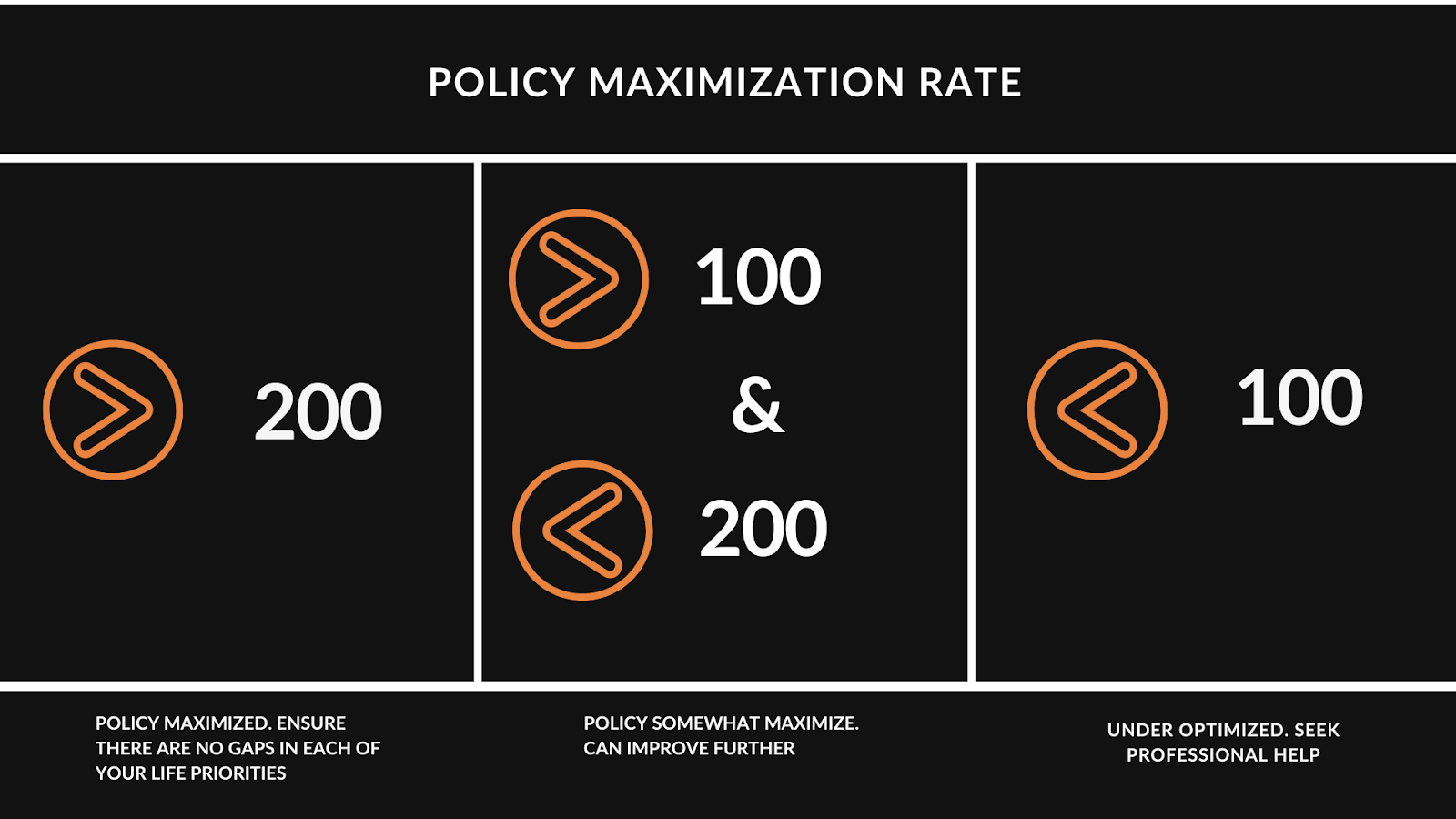

- Identify those policies with PMR rates less than 200.

These are some of the policies that are not stretching your money enough. What do I mean? It means, if your PMR is 155, it means every RM 1 you put in your policy, you are getting RM 155 coverage. So the higher the PMR the better

Here is a guideline for you to refer to.

With this tool, now you can tell which policy is not maximized. The next question you have is “Now that I know which policy is not maximized, How much coverage do I actually need?”, right? Next week I will share this exact topic with you. Share this article with a friend.

Whenever you’re ready, here are 3 ways I can help you to improve your cash flow and double your wealth:

- If you’re still looking for ways to improve your cash flow and double your wealth, I’d recommend starting with

-> Ice Jar – The world’s simplest money management system. This is really the foundation to improve your cash flow and double your wealth. Join 830+ students here

-> Double Your Networth – Join 100+ students go through 4 days intensive webinar to fully understand and apply my 5-step DYN Framework to double your wealth and retire 5-10 years earlier.

- Meet up and clarify your doubts with our coaches.

If you are unsure of where and how to move forward or you are feeling stuck, you can sign up for a complimentary Discovery Call with our coaches HERE.

- Let’s stay connected on social media.

Tune in to my Linkedin, Instagram and Facebook profiles

[Linkedin] [Instagram] [Facebook]