Would You Like To Save 50% of Your Tax Payment?

Would You Like To Save 50% of Your Tax Payment?

(This article is taken from an email post I shared on 2nd Dec 2022)

It is already December. I still remember at the start of this year, looking forward to a brand new start. Before I knew it, 11 months have passed and I am in a holiday mood. I am sure you are in that mood too, right?

But before we turn on our ‘Holiday Mode’, I want to remind you to take advantage of all your tax relief especially if you are earning more than RM 7,000 a month.

I just did a 1-to-1 with 1 of my Double Your Networth student and she was asking me “How do I take advantage of my tax relief?” And I am grateful she ask me this question.

Because sometimes I take for granted that everyone around me knows what to do. Especially since she earns RM 25,000 a month, I know how it feels to pay taxes through her nose.

Would you like a simple tool to help you save 50% tax?

I won’t go through all 15 of the categories but I prepared a simple tool I normally use to plan ahead to see the difference between ‘taking advantage of the tax relief’ vs ‘not taking advantage of it’. Once you download it here, you can see how much money you will save & more importantly you can see your Effective Tax Rate (ETR)

ETR is very important as I previously was misguided when I thought my ETR was 24% when my income was at RM 200k a year. But in reality, when you deduct all the tax relief my ETR was probably at 10% of my total income.

Here is a quick summary of what Personal Tax Relief you can take advantage of (and the typical misses) depending on which category you are in

Single Or Married without kids

- Self – RM 9,000

- EPF – RM 4,000 (if you are under the EPF scheme and not pension scheme)

- Life Insurance – RM 3,000

- Medical Insurance – RM 3,000 (read here on what mistakes to avoid, I wrote a blog on this last year)

- Private Retirement Scheme – RM 3,000

- Lifestyle – RM 2,500 (purchase of books, laptop, tablets and smartphones and internet subscription)

- Additional lifestyle – RM 2,500 (purchase of laptop, tablets and smartphones)

- Domestic Travelling – RM 1,000

- Sports Equipment and Fees for rental – RM 500

- Medical Fees for Parents – RM 8,000 (do ensure you are the only 1 claiming & not claimed concurrently by your other siblings)

- Socso – RM 250

- Vaccination – RM 1,000 (Up to RM 1,000 for yourself)

Married with Kids under 18 years old

- All the above

- SSPN – RM 8,000 (most parents don’t take advantage of this for their kids)

- Ordinary Child Relief – RM 2,000 per child (either parent can claim and not claimed by both parents)

- Lifestyle – RM 2,500 (You can buy laptops, tablets and books for your spouse and kids as well. Since they can’t track, you can even buy laptops, tablets, and books for your nieces or nephew)

- Additional lifestyle – RM 2,500 (if you have more than 1 child, you can claim additional on this purchase of laptop, tablets and smartphones)

- Child Education Insurance – RM 3,000 (read here on what mistakes to avoid, I wrote a blog on this last year)

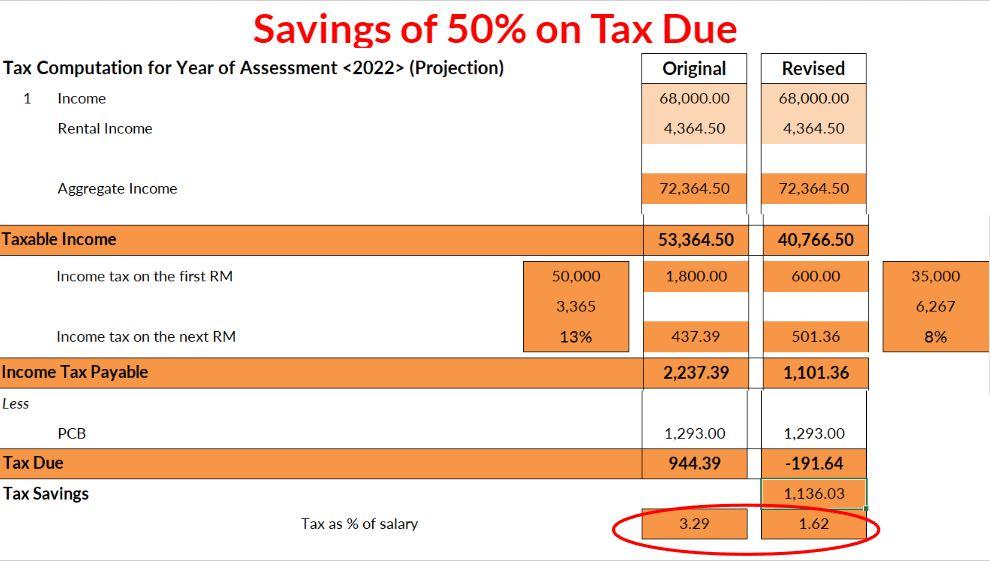

Figure 1

A Case Study to Illustrate

Here is how you can save 50% of your Effective Tax Rate (ETR)

Mr Nair (not his real name) is working for a famous foreign Bank for 5 years. He and his wife have 2 kids. He manages to buy 1 property for investment purposes which he is getting rental income on.

The main strategy to save 50% of your Effective Tax Rate is to maximize all your tax relief (if possible) OR spend/save consciously in areas with tax relief.

For Mr Nair, all he needed to do was to

- Maximize his SSPN by saving for his 2 kids – RM 8,000 (RM 4,000 each)

- Maximize his PRS by saving RM 3,000 to any of the approved Private Retirement Unit Trust

- Take his family for a year-end holiday of RM 1,000 (through approved operators and selected premises here – Item 8)

- Buy a basic smartphone for his son – RM 598

Figure 2

You will notice in Figure 1, his tax bracket dropped from 13% to 8% because his taxable income dropped below the RM50,000 level

Hence he was able to save RM 1,136 on something he needed to do anyway (which was to save for himself and his kids)

In case you are tight on cash, 1 of the method I used was to transfer some of my existing investments / spare cash/emergency funds to my kids’ SSPN or my PRS. The idea is like “Move from your left pocket to your right pocket”

Is this something that benefits you? If yes, do share with me 1 action item you will take before 31st December 2022. Make sure you share this article with those who can benefit.

Next, I will share with you another Tax Saving Strategy (100% legal) by understanding the difference between Employee Tax vs Self Employed Tax and taking advantage of what the government encourages.

Disclaimer: All my sharing here is for educational purposes and are my own personal opinion. It should not be confused with tax advice. You should consult a licensed tax consultant for proper tax planning. I am sharing this with you as my best practice.