Are you Asset Rich but Cash Poor?

Are you Asset Rich but Cash Poor?

“Bro, can you lend me RM 6000, I will pay it back in 2 months,” asked Ben.

I looked across the table at Ben who was sipping his Starbucks coffee. As he raised his Venti cup, the Rolex watch on his wrist was reflecting the low-lit cafe light while he was checking his messages on his iPhone 13 Pro which was exclusively wrapped in a Mont Blanc hardcover.

I was trying to process what he just asked me. Here is a person who I thought was doing very well financially as a regional manager and he is asking me to lend him money?

Something seems off. He didn’t look like he was in any financial distress. Concerned, I asked him: “Ben, is everything all right?” He casually replied: “Yes Bro, I am just having a bit of tight cash flow now, but after I get my bonus in 2 months I can return your money.”

It’s been 3 months now and I have not seen my RM 6000 yet.

Have you come across such friends, or relatives or have you yourself been in a similar position with Ben? From the outside, they carry a good lifestyle image. Their Insta stories paint a fun-filled life with luxury. Continental cars, a big house, fine dining, exotic overseas holidays, designer brands and frequent nightlife with a view of KLCC. But if you know them personally, they are living paycheck to paycheck and one or two months’ salary away from defaulting on their loans.

Similarly, a new study in the US found that 24% of those making $250,000 or more are living paycheck to paycheck.

According to the report, living paycheck to paycheck can mean two things. The first type of people are those who manage to pay all their bills, but at the end of the month, they have nothing left. The second type is those who are struggling to pay their bills. Most high-income people who live paycheck to paycheck have enough to cover their expenses – but not much else. I would strongly recommend them to try out the ICE Jar method as a first step in managing their financial health.

To be fair, they might not even realise that their financial health is in critical shape until it is properly measured.

What gets measured gets managed

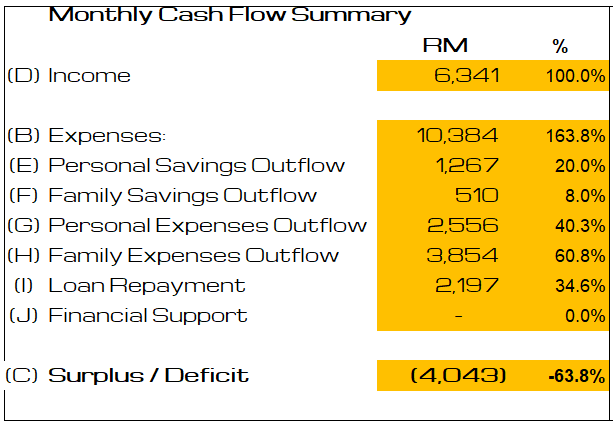

Here is an example. Jason was earning a comfortable income and didn’t know that he was one month away from a crisis if his monthly income stops. As you can see, he is having a deficit of RM 4043 per month to maintain his current lifestyle. How is it possible to spend more than you make then? The simple answer is credit card and personal loan, or in my friend Ben’s case, borrowing from others.

Asset Rich but Cash Poor

This is a typical example of a cash flow summary of a high-income earner. On the outside, they might have many assets (High Net Worth) but they might be struggling with their monthly cash flow.

It is a dangerous situation to be in especially during economic recessions and high inflationary periods as any loss or decrease in monthly income will severely impact your cash flow.

Therefore, it is important you periodically do a financial health check-up to make sure that you are not swimming in debt. Typically, 6 months once review is ideal or whenever you have a major life event (e.g getting a new job, marriage, getting a child).

Have you done your financial health check? Are your financials healthy or you are barely making it through. Do reach out to me if you need any help with your financial health.