How much money should I have to be wealthy? (Free Calculator)

How much money is enough to be wealthy and make us happy? One study suggests that $75,000 per year (RM300,000) is the sweet spot; make anything less or more than that, we will be unhappy.

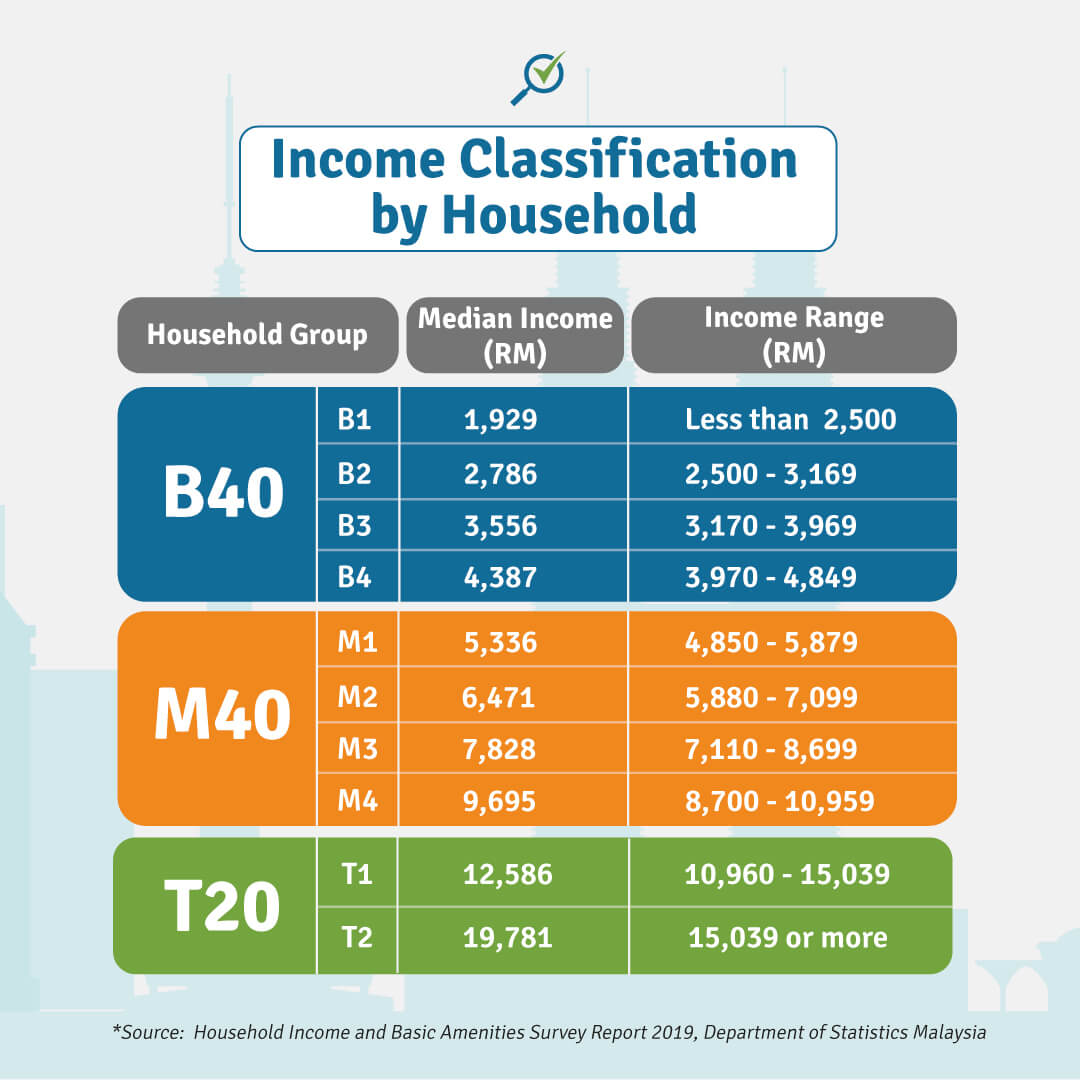

In Malaysia, the government categorises household income in B40, M40 and T20 tiers to make better economic policy decisions.

You might be wealthy and affluent by government standards, but do you feel rich with the rising inflation and cost of living? So what then is the correct number to know how much money should we have to be wealthy?

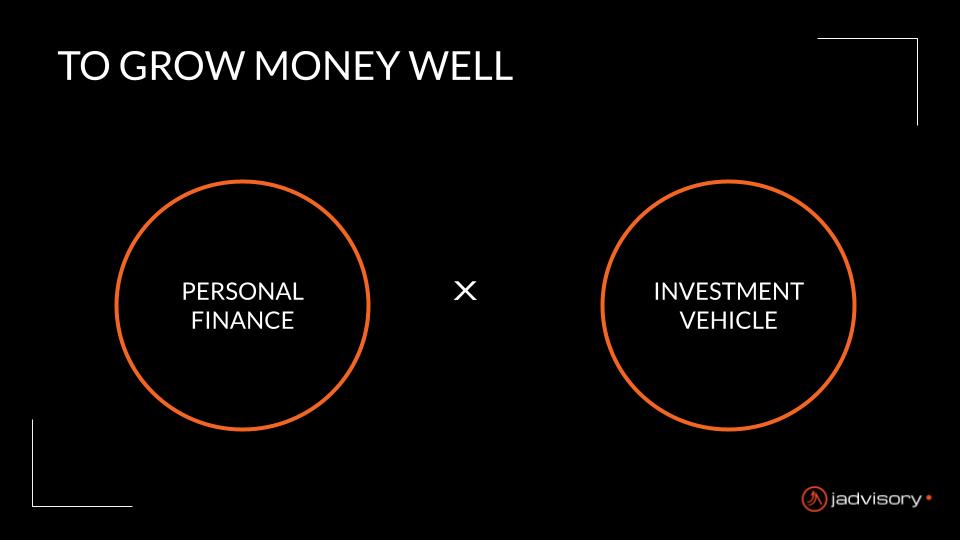

Growing Your Net Worth the Right Way

In reality, wealth is subjective, but growing your net worth essentially comes down to two things:

Sun Tzu once said in his famous book “Art of War”:

“If you know the enemy and know yourself, you need not fear the result of a hundred battles. If you know yourself but not the enemy, you will also suffer a defeat for every victory gained. If you know neither the enemy nor yourself, you will succumb in every battle.”

I know that I am good at growing money. But it is a different mindset from ‘making money. To be good at ‘growing money,’ you need to manage these two things well.

But what most people always focus on is “What’s the best investment ‘𝗼𝘂𝘁 𝘁𝗵𝗲𝗿𝗲’?” “What should I invest in?” “Can crypto make me rich?” “Can investing in properties make me rich.”

All these questions relate to finding the right Investment Vehicle, the thing on the outside.

But great investors never forget to look ‘𝗶𝗻𝘄𝗮𝗿𝗱𝘀’ to see how they are doing financially. What has been working for them so far?

One common misconception inexperienced investors have is that, although the investment vehicle is superb, undervalued and promises excellent returns, not everyone is in a position to invest. Some may put themselves at a higher risk after investing.

For example, some years ago, I was offered a retail lot at Sungai Wang Shopping Complex in Jalan Sultan Ismail. The price was RM 4 Mil for a 1000sq feet unit. It comes with a tenant already paying a monthly rental of RM 20,000.

At that time, I was like, WOW, but I know it was far a BIGGER DEAL I could swallow after looking at my then financial situation. What made it so exclusive was that it was the first retail lot when you came into Sungai Wang Main Entrance (if you are familiar). The investment property promised high foot traffic for any business renting that unit.

So my point here is that it is important to be crystal clear with your current PERSONAL FINANCE situation and the INVESTMENT VEHICLE before making any money decision.

But how many of us are looking into our PERSONAL FINANCE to make money decisions?

Most students and clients I know use their ‘gut feel’. At some point, I am also equally guilty; hence I can relate.

Therefore, instead of just “tembak”, shouldn’t we be using correct data to determine our current situation first before deciding what decision yields the best results for our wealth? Like how all business decisions rely on BIG Data analytics to uncover hidden patterns, market trends and customer preferences. So can you too.

I know it’s a lot of work. So I made a tool to simplify it for you.

Calculate How Much Money You Should Have Now

Take the Millionaire Next Door (MND) test HERE to find out your current financial situation.

I’ll even share with you how to interpret the numbers.

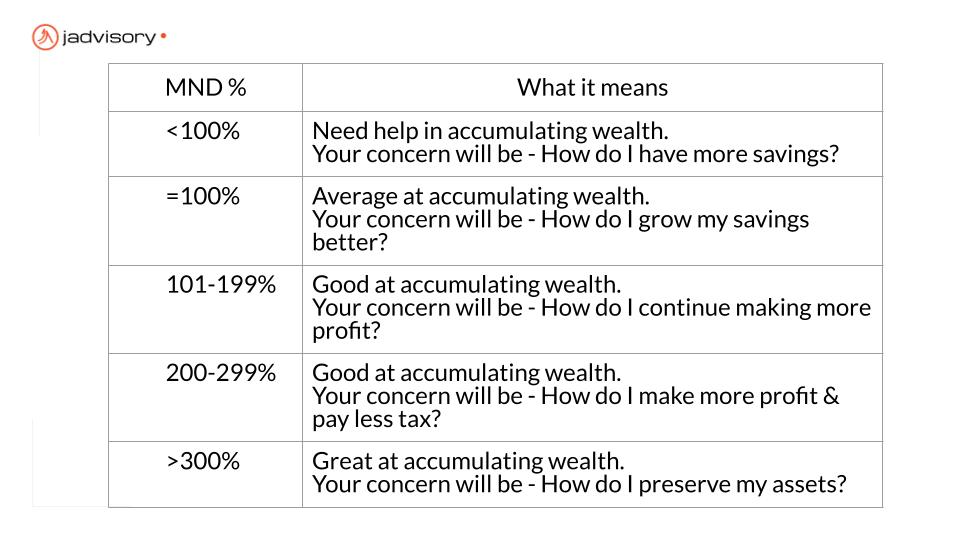

How to Interpret Your MND Percentage

If you have read the book Millionaire Next Door (MND) by Dr Thomas Stanley, you would know this formula is derived from telling whether you are growing your money at a healthy rate. As different people come from different backgrounds, ages, and income levels, it is always very hard to determine how well one is doing? E.g. this is a typical question I usually hear. “How much should I achieve to be RICH?” or “What’s a good Net Worth to aim for one’s age?”

This helps to put a number and physical perspective we can see to finally understand the problem, which our ‘gut’ has been telling us all along, right? Are you satisfied with your MND%? Does the interpretation here resonate with you? Do share with me.

Simplifying Money For You,

Ka Hoe