Is There Such Thing As Low Risk & High Return Other Than Fixed Deposit?

Is There Such Thing As Low Risk & High Return Other Than Fixed Deposit?

Last year, I got asked this common question when FD rates tumbled to an all-time low after Bank Negara announced 4 OPR cuts (OPR = Overnight Policy Rate, this rate influences how banks set their deposit & loan rates) => “How do I get a higher return?”

So, recently when I had to submit my and my wife’s tax submission in August 2021 (yes, we submit so late, that is one of the perks of being a solopreneur & business owner), I had to prepare all the supporting documents for myself and my wife (life insurance premium statement, medical insurance premium statement, SSPN-Skim Simpanan Pendidikan Nasional statements, PRS-Private Retirement Scheme Statements, rental income, tenancy agreements, invoice of repair, maintenance, sinking funds, quit rents and assessments and etc.)

It strikes me that I needed to share this info as I was doing this exercise as it had occurred to me many times, but I didn’t manage to put it down due to the hectic training session in the past 12 months.

So What Was The Trigger?

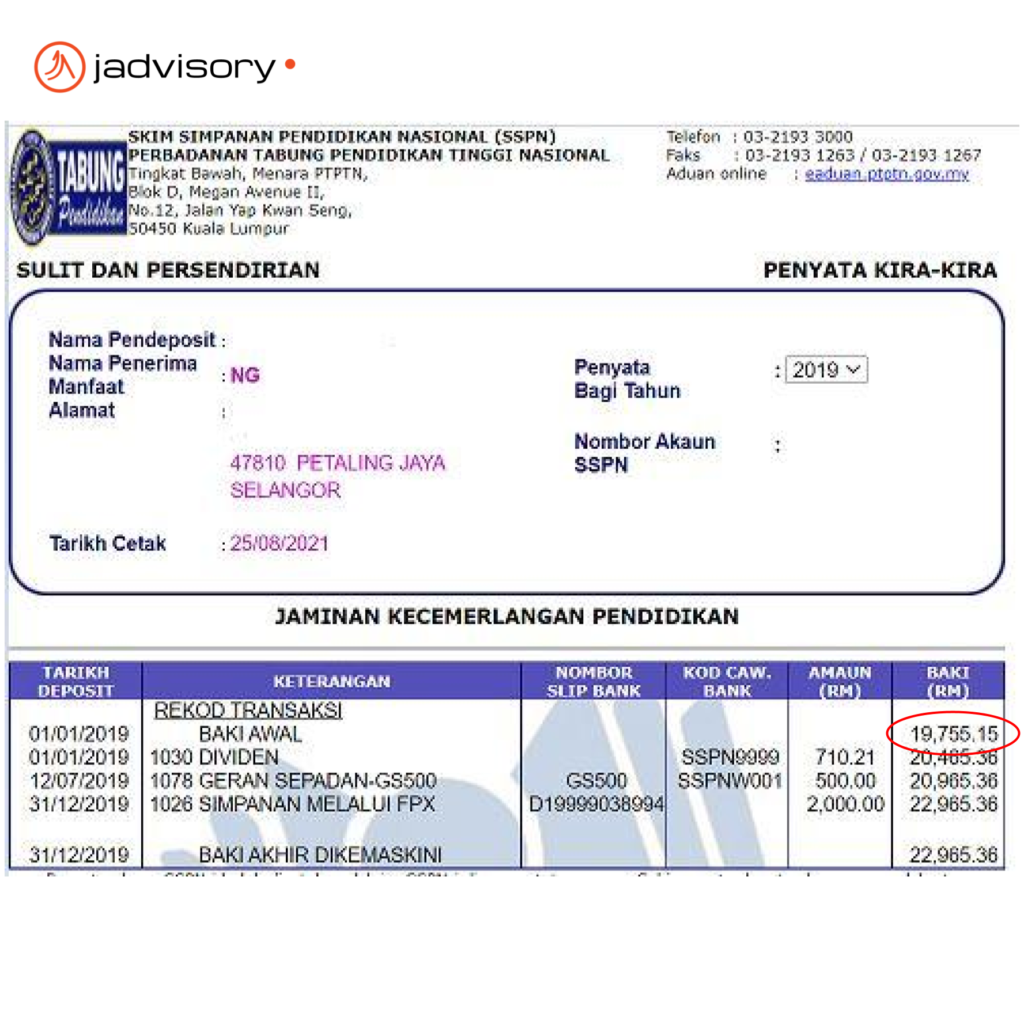

When I was downloading my spouse’s SSPN statement, I saw one line that stood out. It read like this “GERAN SEPADAN – GS500”.

GERAN SEPADAN in SSPN Statement

So when I researched further, I saw this post – https://www.malaysiakini.com/news/473468 – PTPTN was giving out matching grants as an incentive to encourage more parents to save for their children’s education under the National Education Saving Scheme (SSPN)

I heard of this news sometime back but never paid attention to it, as I always feel I won’t fulfil the criteria for the grant. Because previously, I read somewhere that this matching grant was more on helping the B40 group. So when one of my children’s account got the grant, I was quite surprised.

Thus, I went and checked my other two children’s accounts……BUT I did not see the same GERAN SEPADAN.

I didn’t give up; I went to check my portion of contribution for SSPN to my kids to see if ‘my side’ of the kid’s account got it. To my other surprise, I didn’t get it as well. So either my wife has been demoted to B40, or SSPN has tweaked the criteria so that more Malaysians get it.

Did you get it? Leave me a comment below if you did OR know what’s the new criteria.

Realization – Do you know SSPN still pay 4 percent return (dividend) per annum?

Realisation – Do you know SSPN still pay a 4 per cent return (dividend) per annum?

This leads me to my next realisation that I wanted to share with you related to this blog topic. I must say I have a bad habit. I like to calculate the returns on my savings and investment for the ‘fun’ of it. So I can ‘shiok sendiri’ (feel good) and continue to save/invest into what’s right.

Which brings me to the conversation I had with a client sometime back. It goes something like this.

Client – “Ka Hoe, you told me SSPN gives me 4% return? Where got?”

Ka Hoe – “What do you mean? I have been getting for a few years now”

Client – “I just did the calculation just now & I only got like 2+%. If thats the case, I might as well put it in FD”

Ka Hoe – “Well, if is really 2+% is still better than FD, because we get tax deductions. Imagine if you save 8% in your tax deduction, then is a 10% return already. Where can you find a 10% return so easily today?”

Client – “Oh….that’s true, but you check & see whether is really 2+%? Cause if it is then we are being short-changed as we were promised 4% per year”

Ka Hoe – “Sure let me check”

Guess what, my initial reaction was similar to my client. S***, SSPN really ripping us off. They only give us 2+%. But after understanding & analyzing further, here is what I replied to my Client. It went something like this….

Ka Hoe – “Bro, SSPN is not only giving us 4% return but more.

Client – “You sure or not, how’s that possible?”

Ka Hoe – “How did you get your 2+% calculation?

Client – “I took the statement 2020 statement & started using the dividend divide by the beginning balance and multiply by 100. So I took

RM 826.95 / 22,965.36 x 100 = 3.6%.

Isn’t that how you calculate it”

Ka Hoe – “Initially I use the same method you use to calculate. But you notice that the dividend is credited on 1/1/2020. Meaning it is for the 2019 dividend, so we should be using the 2019 beginning balance to calculate.

In this case it is

RM 826.95 / RM 19,755.15 x 100 = 4.19%

Client – “Ohhhh….Now I get it. Wow, they are giving us 4.19% leh. Very good. Really need to put more since now that FD is giving only 2%”

Ka Hoe – “Ya, which I am quite surprised as well. So add in your tax deduction savings, so you get double-digit return. Where can you find such good returns?”

Conclusion

I was quite surprised to see that SSPN is giving us 4+%. Don’t believe me, do your own calculation. I believe the excess on the 4% is the performance return the fund got & shared it among all the depositors.

So now you know where you can potentially get higher than FD returns in this low-interest-rate environment without taking high risk, right?

How To Open an SSPN account?

You can get more information on how to open a SSPN account here.

Previously I went to the SSPN branch to open an account. You just have to bring RM 20 to deposit. The branch was in Kota Damansara Giant, not sure whether the office is still there or not. So this is 1 of the type of savings/investment that you can start, below RM 100. (In case you miss that post, I share on other ways you can start investing with RM 100)

If not, there are 3 options in the link above. You can open an SSPN account online without needing to brave through the risk of getting Covid-19.

Also if you have 3 kids like me, you may want to setup your SSPN account this way

Amount to deposit into SSPN to maximize tax deduction based on Year 2020 (Form B – Resident Individual – Carry On Business) is

Husband – RM 8,000

Wife – RM 8,000

Total – RM 16,000

Husband

Child 1 – RM 2,667

Child 2 – RM 2,667

Child 3 – RM 2,667

Total = RM 8,001

Wife

Child 1 – RM 2,667

Child 2 – RM 2,667

Child 3 – RM 2,667

Total = RM 8,001

WHY SET IT UP THIS WAY?

This ensures fair sharing among the children, and parents have equal access to the tax deduction for individual savings.

CHILD 1 = RM 5334

CHILD 2 = RM 5334

CHILD 3 = RM 5334

TOTAL = RM 16,002

If you are an employee that doesn’t have any business income OR rental income – click on this link below

For Resident Individual – Does not Carry On Business

For more information, go to LHDN’s website on how I found the reference. Click HERE

Can an Individual Without Kids Open a SSPN account?

I am still trying to verify this with SSPN, but when I share this with our J10K Community, our community members verified that they managed to open before even though they don’t have any children. So I will verify and update you guys here.

COMMENT below, your biggest take away & how do you feel after reading this blog.

*Disclaimer – All my sharing here is for educational purposes & are my personal opinion. It should not be confused with financial advice. Different individuals have different scenarios & different needs. Do email me personally about your personal circumstances. As for tax matters, kindly consult your tax consultant for proper tax planning. I am not affiliated with PTPTN in any way & I do not receive any affiliation commission to write this blog.